If you’re looking for a new car, you may consider purchasing a PCP finance agreement. But is PCP car finance deals the right option for you?

PCP finance is a credit agreement and so comes with an Annual Percentage Rate of interest which is the charge for borrowing money.

Here are some things to consider when making your decision:

– How much can you afford to pay each month? With PCP finance, you’ll need to make fixed monthly payments and a final payment (known as the ‘balloon payment’) at the end of the agreement. So make sure you can afford the monthly payments before signing up.

– How long do you want to finance the car? PCP finance agreements typically last between 2 and 4 years. Think about how long you’ll need to finance the vehicle and whether you’ll be able to make the final balloon payment at the end of the agreement.

– What will happen if you want to end the agreement early? With a PCP finance agreement, you may be able to hand the car back and walk away from the deal. However, you may have to pay charges for doing this. Make sure you understand the terms and conditions before signing up.

– What will happen if you want to keep the car at the end of the agreement? You’ll need to make the final balloon payment if you want to keep the car. It is often higher than the monthly payments, so make sure you can afford it before agreeing to a PCP finance deal.

You’ll need to agree on an annual mileage limit at the start of your contract. The lender may charge for any unreasonable damage to the car or for any mileage over the agreed annual mileage. The lower this is, the lower your monthly payments will be. Some PCP agreements have a zero deposit but this will result in higher monthly payments. Once the finance has been agreed upon, provide us with the details of the car dealership.

It’s also often referred to as the Guaranteed Minimum Future Value (GMFV). The Guaranteed Future Value (GFV) is an estimate of what your car will be worth at the end of your finance term, regardless of its true depreciation. Weigh up all these factors before deciding whether PCP finance is the right option for you.

What Are The Main Elements of Personal Contract Purchase?

Personal contract purchase (PCP) agreements are a type of car finance that allows you to buy a new or used car monthly, with a final balloon payment at the end of the agreement.

There are a few things to consider before signing up for a Personal contract purchase PCP finance agreement, such as how much you can afford to pay each month, the length of the contract, and what will happen if you want to end the agreement early.

Here are the main elements of personal contract purchase agreements:

– Monthly payments: You’ll need to make monthly payments towards the cost of the car. The amount will depend on the car’s price and the agreement’s length.

– Final balloon payment: This is a lump sum payment you’ll need to make at the end of the agreement if you want to keep the car. The amount will be agreed upon at the contract’s start and is often higher than the monthly payments.

– Optional final payment: Some PCP agreements have an optional final payment, which is a lower lump sum payment you can choose to make at the end of the agreement. This option is often used if you’re planning to trade in the car or hand it back at the end of the contract.

– Early termination charges: If you want to end your PCP agreement early, you may have to pay early termination charges. These can be high, so make sure you know them before signing up for a PCP deal.

– Mileage limits: Most PCP agreements come with mileage limits, so you’ll need to stay within these if you want to avoid paying extra charges.

Consider all these factors before deciding whether personal contract purchase finance is the right option.

What is an Example of PCP Car Finance Agreement?

Personal contract purchase (PCP) contracts are a type of car finance that permits you to buy a new or used car monthly, with a final balloon charge at the end of the contract.

There are rare things to believe before signing up for a PCP car finance agreement, such as how greatly you can afford to spend each month, the stature of the contract, and what will happen if you want to end the contract early.

Here’s an example of how a PCP car finance contract might work:

– You decide to finance a car worth £10,000 over three years.

– The deposit amount is £1,000, and the monthly payments are £200.

– At the end of the three years, you can make a final balloon payment of £3,000 to keep the car or hand it back without further payments.

If you choose to keep the car, you’ll need to pay £13,000 throughout the agreement. It includes the deposit, monthly payments, and final balloon payment.

If the value of the vehicle declines quicker than expected during the loan term, it can simply be handed back to the finance provider. If you decide to hand the car back at the end of the agreement, you won’t need to make any further payments. However, you may have to pay early termination charges.

Consider all these factors before signing up for a PCP finance agreement to make sure it’s the right option for you.

What Are The Options Once The PCP Finance Deal Comes to an End?

A few options are available if you’re coming to the end of your contract purchase PCP finance deal.

You can:

– make the final balloon payment and keep the car,

– trade the car in for a new one, or

– hand the car back and walk away without any further payments.

You’ll need to make the final balloon payment if you decide to keep the car. It is often higher than the monthly payments, so make sure you can afford it before agreeing to a PCP finance deal.

If you want to trade the car for a new one, you can use any equity in the car as a deposit towards the new vehicle.

You may have to pay early termination charges if you decide to hand the car back. These can be high, so make sure you know them before signing up for a PCP finance deal.

Consider all your options before coming to the end of your PCP finance deal to make sure you choose the right one for you.

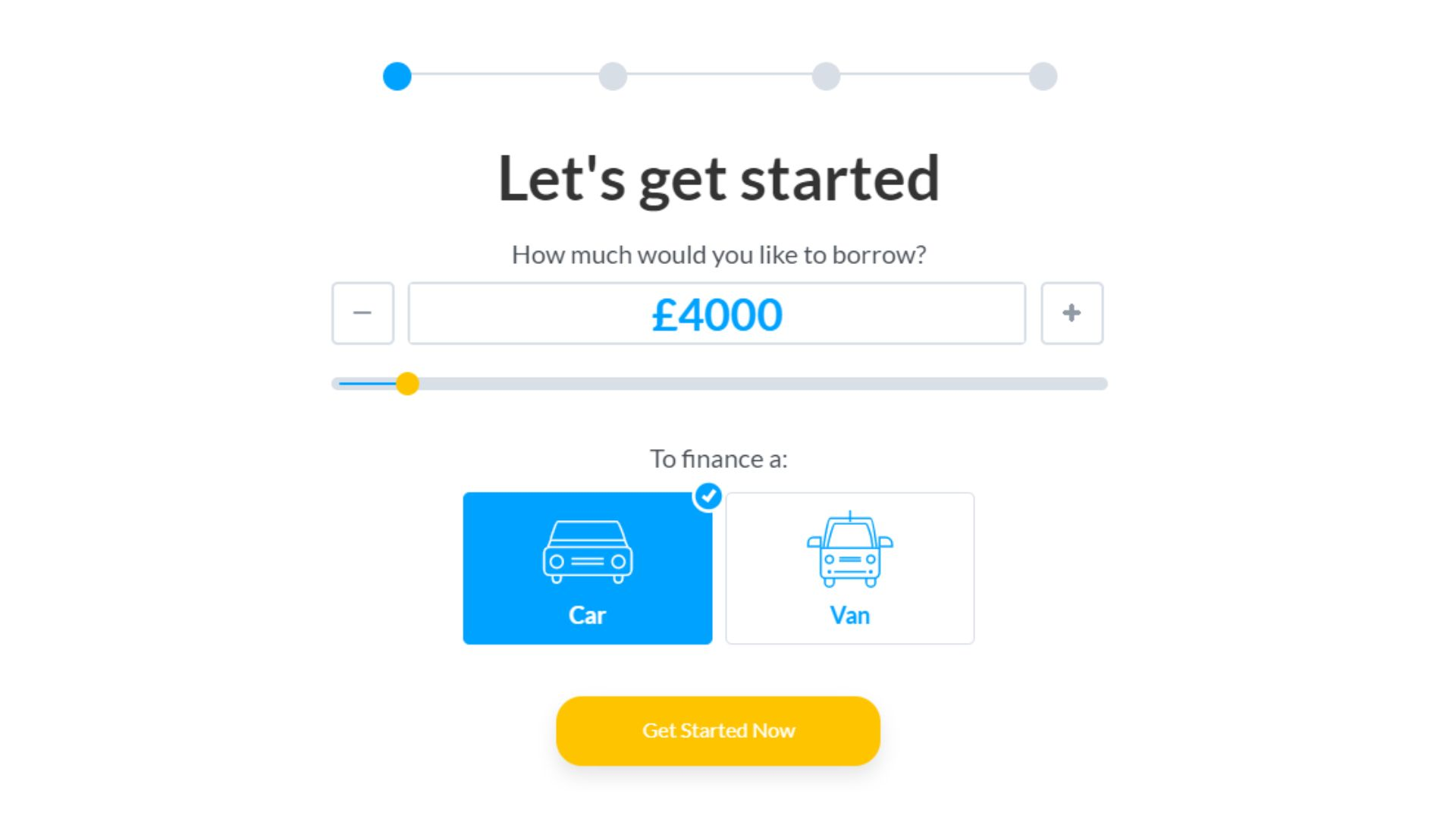

How Will You Determine The Amount You Can Borrow for Cars on PCP?

Before signing up for a PCP finance agreement, there are a few things to consider, such as how much you can afford to spend each month, the length of the contract, and what will happen if you want to end the contract early.

Here’s an example of how much you might be able to borrow for cars on PCP:

– You will need to have a deposit of 10% of the car’s value.

– For a new car worth £10,000, this would be a deposit of £1,000.

– The monthly payments would be based on the car’s remaining value after the deposit has been paid.

– In this example, you would need to finance £9,000 over three years.

– This would give you monthly payments of £250.

– At the end of the three years, you can make a final balloon payment of £3,000 to keep the car or hand it back without further payments.

If you choose to keep the car after the end of the contract, you’ll need to pay a total of £13,000, including the deposit, monthly payments, and a final balloon payment.

Then, if you want to exchange the car for a new one, you can use any equity in the car as a guarantee for the new vehicle.

If you decide to hand the car back at the end of the finance agreement, you won’t need to make any further payments. However, there may be early termination charges that apply.

Make sure you consider all these aspects before signing up for cars on PCP to ensure it’s the right choice for you.

What Are The Advantages of Car Finance on PCP?

There are several advantages to car finance PCP, such as:

– You can spread the cost of the car over some time.

– You can make lower monthly payments by deferring some of the cost to a final balloon payment.

– You have the option to trade the car in for a new one at the end of the agreement.

– You may be able to negotiate a lower interest rate than other types of car finance.

Consider all these factors before signing up for car finance PCP to make sure it’s the right option for you.

How Does Car PCP Finance Differ From PCH and HP?

Car PCP finance is similar to other types of car finance, such as personal contract hire (PCH) and hire purchase (HP). However, there are some key differences that you should be aware of before signing up for a car finance agreement.

– Car PCP finance deals usually last for two or three years, while PCH and HP agreements can last up to five years.

– You will need to deposit with car PCP finance, but this is not always required with PCH and HP.

– With car PCP finance, you can trade the car for a new one at the end of the agreement. It is not usually possible with PCH and HP.

– You may be able to negotiate a lower interest rate with car PCP finance than with PCH and HP.

Consider all these factors before deciding which car PCP finance option is right for you.

Who Offers PCP Finance Deals?

Several different lenders offer car PCP finance deals. Here are some of the most popular:

– Ford Credit

– Volkswagen Bank

– BMW Financial Services

– Audi Financial Services

– Mercedes-Benz Financial Services

Before signing up for a car finance agreement, compare offers from different lenders to find the best PCP finance deals for you. CarFinanceMarket.co.uk is a great place to start your search. CarFinanceMarket.co.uk is authorised and regulated by the Financial Conduct Authority. We are an independent car finance broker, and we can help you find the best PCP finance deals from various lenders. So contact us today to get started.

What You Need To Get PCP Finance Car With Car Finance Market?

If you’re looking to get a PCP finance car with Car Finance Market, there are a few things you’ll need:

– A deposit of 10% of the car’s value

– A good credit score

– A steady income

If you have all of these things, then you should be able to get a PCP finance car with Car Finance Market. So contact us today to get started. We can help you find the best PCP finance deals from various lenders and get you into your new car in no time.

Conclusion

Car finance PCP can be a great option if you’re looking to spread the cost of a new car over time. However, comparing offers from different lenders is essential and ensuring you understand all the terms and conditions before signing up for an agreement. Choose the car finance option PCP deals with finance providers that are right for you. Car Finance Market is a great place to start your search for the best PCP car deals UK based. We are an independent car finance broker who can help you find the best deals from various lenders. So contact us today for more info about car deals and to get started early.